|

|

Calculating the Cost of the Problem

Salespeople can do a thorough job of establishing and communicating the symptoms and causes of customers' problems, present viable solutions to those problems, and still walk away from the engagement empty-handed. This outcome most often occurs when salespeople ignore a crucial piece of the diagnostic process - connecting a dollar value to the consequences of the problem.

Problems run rampant in organizations. Some are not significant enough in consequences or risk to address; others must be addressed because their consequences or risks are too high. The fact that a problem exists is not enough to ensure change. When the customer does not know the actual cost of a problem, the success of winning the enterprise sale is severely compromised.

Typically, customers do not quantify the costs of complicated problems on their own. The main reason for this, as we saw in Chapter 2, is that most customers simply don't have the expertise required to fix those costs. Even when they do attempt to quantify their problems, they usually focus on the surface costs and tend to overlook the total cost.

Salespeople also tend to shy away from fixing costs. Many complain that it is too hard to determine, but we find that the real reason is that they are afraid that the cost of the problem will be too low to be addressed and the engagement will be over. They are reluctant to do anything that might interfere with "going for the yes." This is always a possible outcome, and it is a legitimate one. If the cost of a customer's problem does not justify the solutions being offered, the professional will acknowledge that reality and (in the spirit of "always be leaving") move on to a better qualified customer. If this happens too often, the salesperson and his or her organization have a larger problem - solutions are too expensive in terms of the value they offer customers.

Another common objection to cost calculation that we hear from salespeople is that their offerings are not meant to solve problems. They say that they provide new opportunities; therefore, they can't fix the costs. This is not a.valid objection. There are no free moves in business. There are always costs present in every decision. Even when a solution offers a new capability, there is still a cost if the customer chooses not to adopt it.

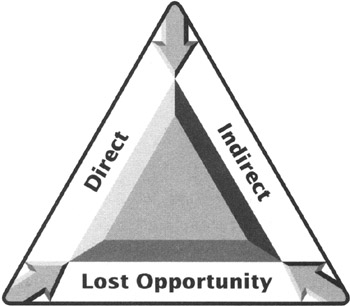

When salespeople explore the total cost of a problem, they need to use a combination of three types of figures:

-

Direct numbers: Established or known figures.

-

Indirect numbers: Inferred or estimated figures.

-

Lost opportunities: Figures representing the options that customers cannot pursue because of the resources consumed by the problem.

When we talk about the total cost of the problem, we are not saying that you must establish a precise figure. Rather, the cost must be generally accurate. Calculating costs is a process similar to the navigational method known as triangulation. By sighting off of three points - the direct numbers, indirect numbers, and lost opportunities - we can arrive at a cost that is accurate and, most importantly, believed by the customer (see Figure 5.2).

This is accomplished in two steps. First, we salespeople need to provide a formula that is conceptually sound. Second, we must ensure that the numbers plugged into that formula are derived from the customer's reality, not the salesperson's. We know we have successfully completed these steps when our customers are willing to defend the validity of the cost among their own colleagues.

The following example shows how a cost conversation works. A salesperson in the shoplifting detection equipment industry calls on independent pharmacies. He engages the owner of a drugstore with revenues of $1.5 million, who is experiencing the industry average shrinkage of 3 percent. This tells the salesperson that the store is losing $45,000 annually to some combination of customer theft, employee theft, and sloppy inventory management. The store manager, who does not believe that the store is experiencing any significant customer theft because the store is in a "better part of town," is not interested in the salesperson's offering.

The salesperson agrees with the customer's point (atmosphere of cooperation) and then asks an Indicator question, "Do you ever notice empty packages on the floor?" The store manager replies, "You have a point there, but it's not enough to be worried about." "Probably not," the salesperson replies and then asks the next question to establish an indirect number. "Out of every 100 people in this community, how many do you think would shoplift?" The curious manager replies, "One percent, 1 out of 100."

The salesperson now asks for a series of direct and indirect numbers, such as the number of buying customers in the store each day and the ratio of buying customers to browsers. They yield a figure of 533 people in the store each day. The salesperson asks, "What do you think the average cost of a shoplifting incident would be?" The manager replies, "$15."

From this information, the salesperson calculates that there are five shoplifters in the store each day, and the average daily loss is $75. Further, the store is open 365 days each year, making the annual loss $27,000 - a believable figure in light of the store's $45,000 annual shrinkage.

The detection equipment costs $15,000 to install and $2,000 per year to operate. Subtracted from the cost of the store's problem, this yields a positive return of $10,000 the first year and $25,000 in subsequent years. Over three years, the lost opportunity is $20,000 per year. [2]

As you can see, we develop the data used to determine costs the same way we explore problems - through the process of diagnostic questioning. The answers to our questions tell us whether our customers have the resources and willingness to solve their problems. More importantly, the process of answering questions allows our customers to reach their own conclusions in their own time. Further, the fact that the customer provides the data enhances the credibility of the cost conclusions that result. This creates a high level of buy-in. It is also more compelling and accurate than the generic cost/return formulas and average industry costs that we so often find in conventional sales presentations.

Remember, it is the responsibility of the sales professional to develop the "cost of the problem" formula. It is a critical component of the quality decision process that they bring to their customer. The customer does not have the expertise or the inclination to put such a formula together. It will provide you with a key differentiator.

The final element of the Diagnose phase is to determine the problem's priority in the customer's mind. This is one crucial test of the significance of a problem's consequences that salespeople often overlook. The fact that a problem's costs are substantial in the salesperson's eyes does not guarantee that the customer feels the same way or will attempt to resolve it.

First, the cost may be an accepted part of doing business. A retail chain includes a line item for inventory shrinkage in its annual budget; a manufacturing plant considers some level of defects acceptable. Unless the cost exceeds acceptable levels, salespeople may well find that the customer will not feel the need to make a decision to change.

Second, even when costs do exceed acceptable levels, they must still be compelling in light of the other critical issues vying for the resources of the organization. If, for example, a customer is confronting a shrinking market for the goods or services the salesperson's offerings address and, as a result, has decided to leave that business, there is little reason to invest additional resources no matter how compelling the cost savings.

This is why it is so important to ask the customer to prioritize the problem and its costs before moving out of the Diagnose phase of the sale process. Again, this information is developed by asking questions, such as conversation expanders (see Figure 5.3).

Cost Quantification

Have you had a chance to put a number on ... ?

What does your experience tell you ... is costing?

Can you give a ball park number as to what ... costs?

Cost Prioritization

How does ... compare to other issues you are dealing with?

Does it make sense to go after a solution to ... at this time?

When you consider all the other issues on your desk, where does ... fall?

Figure 5.3: Conversation Expanders - Cost of the Problem

[2]This example is based on an actual situation in which a client of ours used a similar cost analysis to sell its equipment to a national chain of drugstores.

The topics covered herein concern solution sales, consultative sales, and consultative selling.

|

|

|